For several years the Japanese government and, more specifically, the new digital agency has been trying to sell the public on the My Number system, which assigns a 12-digit ID number to everyone who lives in Japan. Assigning the numbers was the easy part: bureaucrats generated the numbers and sent them out on small paper cards. The idea was that these would be used, as are social security numbers in the U.S., for various government functions to streamline procedures, such as filing tax returns, using national health insurance, and applying for public services. The problem has always been that a certain cross-section of the public doesn’t feel comfortable with the number, since it smacks of government overreach and control, and, despite the ruling party’s continuing success at the polls, the public for the most part doesn’t trust the authorities, which is understandable. Twenty years ago, for instance, the welfare ministry discovered it had lost millions of pension records, thus necessitating a years-long retrenchment of the whole system that inconvenienced thousands of retired people. How would such officials handle numbers that in principle were supposed to connect to the most personal data the government keeps under virtual lock and key?

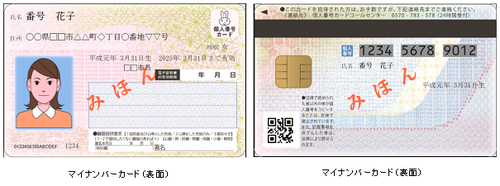

Consequently, the relevant authorities have had their hands full trying to proceed to the next step of the My Number system, which is to get dedicated My Number cards in the hands of everyone in the country. The card is more elaborate than the little paper thingy, which simply has the holder’s name, address, and number printed on it. The real cards, which are plastic, look like a genuine piece of ID, with a photo of the holder and a chip that makes it usable on digital devices to connect to a central database. This, apparently, is a bridge too far for many people, and the penetration rate for card application has been much lower than the government had expected. According to various media reports, as of May, only 44 percent of people who should have the cards have applied for and/or received them, which is pretty sad because the expressed goal is to have cards in everybody’s hands by the end of fiscal 2022.

I received mine about a year ago. Call me an easy touch, but I think the basic concept is good. As an American, the My Number card just sounds like a supercharged social security card, which many Americans find scary, too, but as someone who actually pays their taxes in full and on time, I figure I have nothing to fear from Washington (unless they read this blog, which I doubt), so, naively perhaps, I don’t really think the Japanese government is going to come after me. (By no means do I speak for all foreign residents.) Having an all-in-one card that I can use to pay my taxes, handle my health insurance payments, and access government documents sounds like a fine idea. And it was a painless, easy process. After receiving an application in the post from my local government I sent it in with a photo and a few months later went to my local city office to pick up the card. There I registered a password and received a short lecture on how to use the card. That was it. In the past year, I’ve used the actual card only once (the number itself I’ve used several times), when I applied for my vaccination certificate for overseas travel.

But a week or so ago I read that the government had implemented an incentive program to boost applications and found that, although I already had the card, I could still earn up to ¥20,000 worth of points if I registered it for various services. Wanting to learn more I looked on the internet and found a May 18 article in the Tokyo Shimbun that explained the program in detail.

The first thing that struck me was that it will cost ¥1.8 trillion, which sounded like a lot. The second thing is that the application for points can only be done online, which means older people could have trouble carrying it out, if the stereotype is true. Knowing this, the government has enlisted some 30,000 post offices and cell phone stores throughout Japan to assist anyone with the application process, but that still means the digitally disadvantaged have to go somewhere to get their points. More significantly, the points can only be used digitally, since they will be deposited into existing e-money plans and apps. So while the application for the actual card is disarmingly analog, in order to enjoy the incentive, the process becomes more dauntingly digital. Of course, to those who are comfortable with technology, this process should pose no problem since all they have to do is sit down at their computer or phone and go through the steps, but further reading of the Tokyo Shimbun article showed that this wouldn’t necessarily be the case.

The point incentive is simple enough. Anyone who applies for a card can receive 5,000 points after the card is issued, though they have to apply separately to receive them. In addition, anyone who registers their new card for health insurance payments can receive an additional 7,500 points; and another 7,500 points are granted to those who register their bank information. Deadline for the card application to receive points is December of this year, and the deadlines for applying for points for insurance and bank info is the end of next February. According to Tokyo Shimbun, the government already offered a point system for applying for the car during its initial promotion push, from Sept. 2020 to Dec. 2021, but for some reason when I applied for my card I was not made aware of these points. However, even though I already have my card it seems I can still apply for the new 5,000-point incentive. As it stands, slightly less than 50 percent of people who have already applied for cards have also applied for points, so I guess I’m not alone.

From what I gather the reason many people don’t apply is not because, like me, they didn’t know about the points, but rather that they just can’t be bothered, since the infrastructure needed to not only use the dedicated My Card is not in place nationwide, but use of the points will be limited. The point system incentive has two purposes: Get people to apply for the cards, and increase the use of e-money. Though e-money usage has increased significantly in Japan in recent years, it hasn’t reached a level that justifies the kind of effort needed to apply for the points. Tokyo Shimbun implies that applying for the points is a complicated process that requires making separate applications to e-money plans, of which about 90 are eligible.

There are other disincentives. Medical institutions have to set up a special card-reading apparatus before they can accept the My Number card for paying medical fees through national insurance, and Nihon Keizai Shimbun reports that as of July not even 30 percent of hospitals, clinics, pharmacies, and doctor’s offices had done so. Moreover, the fee for using the card is higher than the fee for not using it. Whenever you go to a clinic or hospital for medical treatment and pay with the My Number card, the accountant bills the government insurance system, and that includes an initial monthly visitation fee of ¥70, which means the patient pays about ¥21, or 30 percent of the fee. If the patient revisits the medical institution in the same month, the institution charges the government ¥40, and the patient pays ¥12. When a new month starts the cycle starts over again, because medical institutions bill the government on a monthly basis. However, if the patient just uses their regular insurance card, meaning they don’t use the My Number card, the initial visitation fee is only ¥30, meaning the patient pays ¥9.

Obviously, if people know about this, they aren’t going to use their My Number card to pay their medical fees (including for pharmaceuticals), and opposition parties have questioned the government on the rationale for this system, since one of the points of digitalization is to reduce administrative costs. So in October the system will change: ¥20 for the first visit using the My Number card (patient pays ¥6) and no subsequent payments for repeat visits the rest of the month; while use of regular insurance card for first visit will increase to ¥40 yen for initial visit (patient pays ¥12). As to how much this new system will reduce administrative costs, it all depends on how many medical institutions adopt the My Number card system for handling payments. At present there seems to be no mandate, so if the institution can’t be bothered, then they’re not going to buy card readers and attendant software and equipment. After all, they lose nothing by sticking with the regular insurance card system since they just bill the government for everything.

The medical insurance story just goes to show how incoherent the My Number card system is at the moment, and also may point to the probability that these point incentive programs aren’t going to boost applications by that much. There are too many variables and exceptions to both the application process and the actual use of the cards to make people think that having one will be an advantage, so unless the government makes the cards mandatory, it’s unlikely that the penetration rate will ever reach 100 percent. But first they have to guarantee people’s privacy, which they seem unable or unwilling to do. Social media is filled with doubters who think that applying for a card is tantamount to selling their personal data. The mayor of Akashi in Hyogo Prefecture said as much in a recent tweet, where he mentioned the 20,000-point incentive and wondered why the government was wasting so much money to sell a system it had promoted as being beneficial to everyone. Either provide it in a way that makes people accept it or just drop it.